Tax Effective Life Insurance for Property Investors

Relevant Life

What is Relevant Life?

Relevant life cover offers a tax efficient way for an employer/Business Owner, usually a small business, to provide life cover for individual employees. It offers financial protection for the employee’s spouse, partner or dependants, paying out a cash lump sum if the employee dies or is diagnosed with a terminal illness during the policy’s term.

Premiums are paid by the employer and are usually viewed as an allowable business expense by HMRC. This means both the premiums and any benefit paid are eligible for relief from income tax, corporation tax and national insurance contributions.

The main benefit therefore is for directors is this being paid by the business pre-tax rather than out of their own pocket post tax.

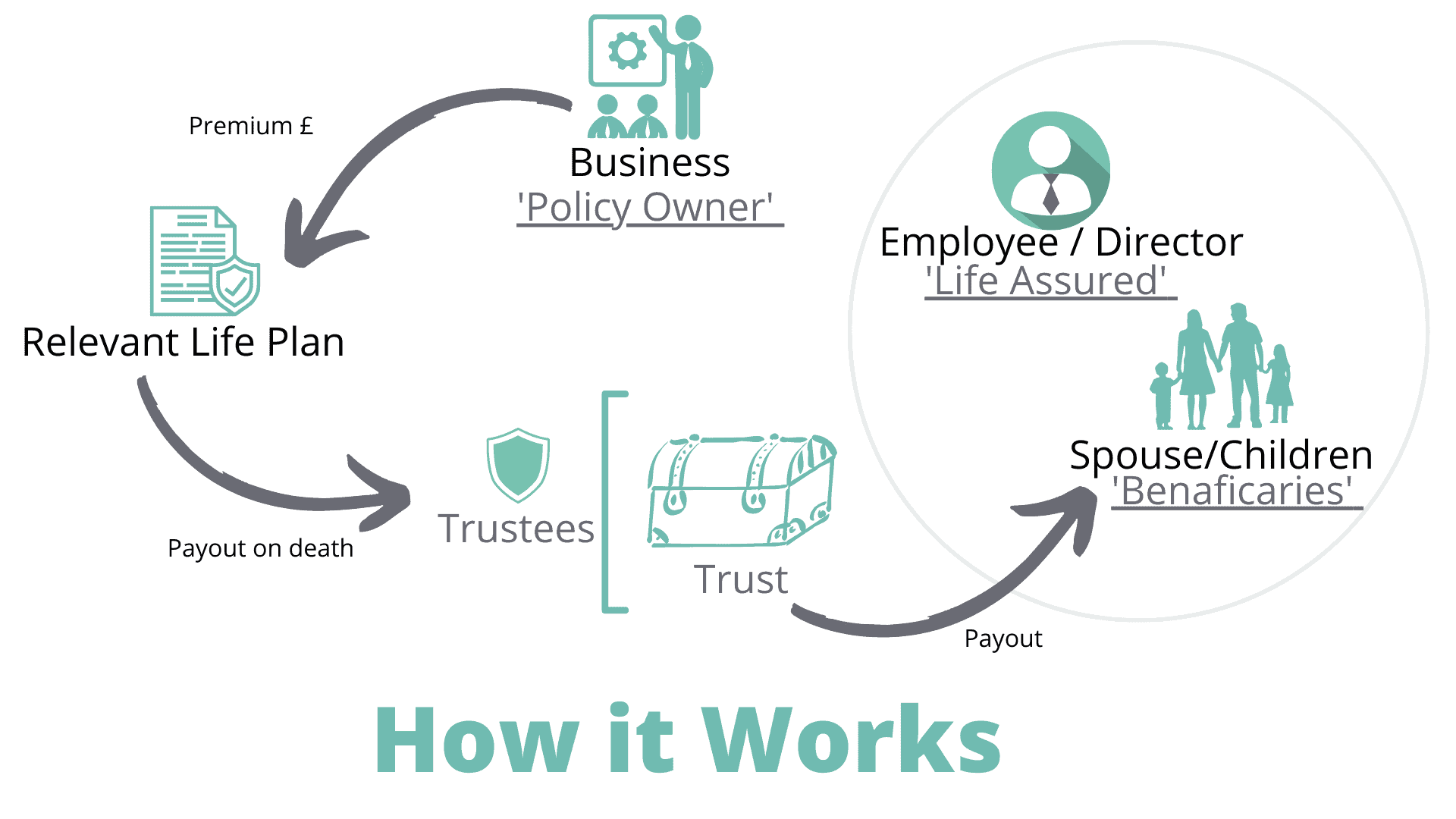

How it works

The business pays £X a month of the policy term

Life assured dies during the term

Trustees make a successful claim

Trustees pay the beneficiaries

Why use it? Tax Benefits

*Based on current tax rules

First and foremost, the main advantage is cost saving to an employee or director is paying it post tax vs pre-tax through the business. See the below example:

Non-Relevant life plan (Post tax out of your own pocket)

Relevant Life Plan (Pre tax)

Annual Premium

£1,000

£1,000

Employee National Insurance Contribution (assuming 2%)

£34.48

None

Income Tax (assuming 40%)

£689.65

None

Dividend Tax

None

None

Gross earnings needed

£1,724.13

£1,000

Employer National Insurance Contribution (assuming 13.8%)

£237.93

None

Total gross cost

£1,962.06

£1,000

Less Corporation Tax (assuming 19%)

£372.79

£190

Tax-adjusted total cost

£1,589.27

£810

The main take away from the above example is for a person to pay for a policy themselves it would cost them £1,589.27 every year, the cost via a limited company is £810.

Other tax benefits

- No assessment of premiums on the employee as benefit in kind or otherwise.

- Premiums paid by the employer are usually viewed as an allowable business expense by HMRC.

- Premiums and any benefit paid are eligible for relief from;

- Income Tax

- Corporation Tax

- National Insurance contributions

- Benefits do not count towards the lifetime allowance for pension purposes.

- In most cases benefits are paid free of inheritance tax.

The plan will have no cash in value at any time and will cease at the end of the term. If premiums are not maintained, then cover will lapse.

Akash Desai – Principal Protection Adviser OnPoint Mortgages